This is the first of three parts.

Draft unfinished series bug

The spring day in 2016 that movers and shakers in the veterinary community gathered on the campus of Michigan State University was sunny, mild and filled with promise.

United by the view that student borrowing in the United States to finance veterinary school had escalated to an unacceptably unaffordable level, the 180 participants came to brainstorm ways to wrestle it down. To, as the summit was named, "Fix the Debt."

Dr. Matt Holland, then freshly installed as president of the Student American Veterinary Medical Association, and approaching his final year of study owing well into six figures, felt optimistic and grateful. "I really appreciated that leaders in the profession, people I looked up to, thought it was worth their free time — their extra time and energy that they could have used on something else — to address this problem," he recalled. "I remember people saying things like, 'Oh, nothing like this has ever happened before.' It felt very full of potential."

The goal of the summit was to identify steps to lower student debt so that it would be better aligned with starting pay. The so-called debt-to-income ratio had reached about 2-to-1, meaning the sum owed by the average new veterinarian was two times their expected annual starting income. That is double the 1-to-1 debt-to-income ratio considered prudent for most people. Summit-goers, following the recommendation of Michael Dicks, then chief economist of the American Veterinary Medical Association, set a target ratio of 1.4-to-1, based on the premise that people with graduate degrees have better earning potential than those with only undergraduate degrees.

Five years later, the goal remains elusive; the progress, modest. On the plus side, the debt issue is widely known and acknowledged in the profession, a few schools have managed to hold the line on tuition, and resources have proliferated to help students with personal financial decisions and debt management.

But by the most telling measures — the scale of debt, the overall cost of education and, most importantly, the debt-to-income ratio — nothing is fixed. While demand for veterinarians is high and incomes are up, so is debt. For new veterinarians as a group, the imbalance of debt and income seems stuck at 2-to-1, and that big-picture snapshot obscures a disquieting trend: A greater share of new graduates owe nothing, while some have astronomical debt, suggesting that the profession's newest cohorts are comprised increasingly of haves and have-nots.

Many Fix the Debt participants readily admit disappointment. "We were looking for a whole lot more from the summit than what has happened," said Dr. Mary Beth Leininger, a former AVMA president and member of the AVMA's school accreditation body, the Council on Education; and a practice co-owner for nearly three decades. Leininger, now retired, donated to help stage the $100,000 event.

Another donor, Dr. Dan Lorimer, said, "I kind of felt like we had a nice symposium, honestly, and then everybody went about their way." He laughed dolefully and added, "We've increased the exposure to this [issue] and there's been some writing about it, but I don't think anything significant has been done."

Lorimer, a Michigan State alumnus and boarded ophthalmologist who owns stakes in 400 practices, sees each side of the debt-income equation pointing to the other for the solution: "The universities think practices should just pay higher salaries, and practices think the universities should lower tuition. And the students are caught in the middle. ... I just think the system is broken."

Mind-numbing numbers

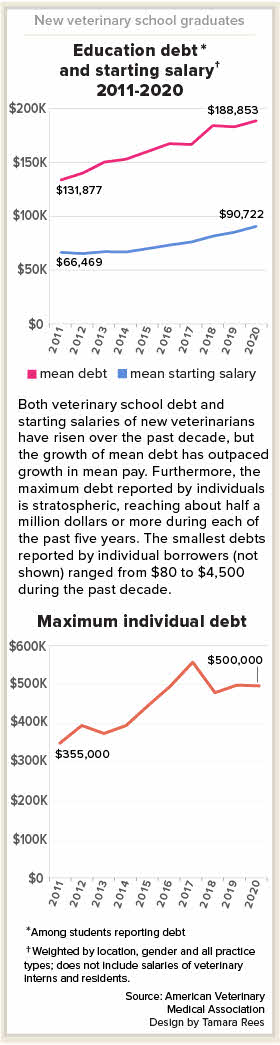

How much do today's U.S. veterinary graduates owe? The average veterinary-school debt among borrowers in 2020 was $188,853, according to an AVMA survey of fourth-year students shortly before they graduated.

While a handy proxy, the single figure doesn't capture the many dimensions of the issue. It doesn't, for example, show the extreme range that individual borrowers reported owing — as low as $1,004 and as high as $500,000.

It doesn't include the usually higher-than-average debt of the one in four American veterinary students who go to school outside the country — to places such as Ross University School of Veterinary Medicine on the Caribbean island of St. Kitts, where the veterinary program is overwhelmingly comprised of U.S. citizens. (A 2018 survey by the AVMA found that the average debt among indebted graduating veterinary students at Ross University and at St. George's University in Grenada, also in the Caribbean, was $295,467.)

The figure doesn't include the debt that students incurred before they entered veterinary school. (The average among the 40% of veterinary school applicants in 2020 who had undergraduate debt was $33,459, the AVMA found.)

At the same time, one out of six veterinary school graduates that year reported owing nothing. If their zero balances are factored in, the average veterinary-school debt of the class of 2020 is just over $157,000.

Choosing a figure to represent income of new veterinarians also is tricky. Calculating the starting pay based on the full spectrum of jobs — in urban and rural private practice, government, industry, nonprofit work, academia and advanced education — brings down the average considerably because interns and residents are paid notoriously little. Starting salary calculations usually exclude the anomalously low wages of those in advanced training.

Choosing a figure to represent income of new veterinarians also is tricky. Calculating the starting pay based on the full spectrum of jobs — in urban and rural private practice, government, industry, nonprofit work, academia and advanced education — brings down the average considerably because interns and residents are paid notoriously little. Starting salary calculations usually exclude the anomalously low wages of those in advanced training.

The AVMA also weights its average salary calculation by location, gender and all practice types, explaining: "The veterinary profession is so complex that an increase or decrease in salaries could signal a demographic change, or more practitioners from lower-paid specialties entering the profession, even though within those demographics or specialty areas, incomes could be increasing."

AVMA's mean weighted annual pay calculation for new veterinarians in 2020 was $90,722. With the average debt among borrowers at $188,853, that makes for a debt-to-income ratio of roughly 2-to-1. (The AVMA has a more precise way of figuring debt-to-income ratio: It calculates the ratio for each student reporting debt and expected income, then finds the mean of that group. For borrowers in the class of 2020, the ratio is 2.1-to-1 with either method.)

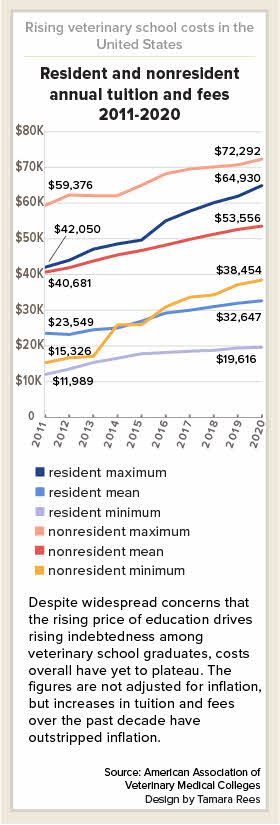

Reporting the cost of veterinary education likewise is complicated. There are 33 veterinary schools in the U.S. and 21 in other countries that are AVMA-accredited. In the U.S., public institutions have two tiers of tuition, one for residents, one for nonresidents. Private schools charge a single rate. Public or private, the price of attending veterinary school isn't captured by tuition and fees alone. Insurance and supplies are extra, never mind living expenses like housing, food and transportation.

Using tuition and fees as a proxy for overall cost, though, figures from the American Association of Veterinary Medical Colleges show that the trend during the past decade is inexorably up, at more than twice the rate of inflation. In nominal dollars, average resident tuition went up more than 38% from 2011 to 2020; nonresident tuition, which includes tuition of private schools, more than 31%. Inflation over the same period was 15%, according to U.S. Bureau of Labor Statistics Consumer Price Index data.

In 2020, AAVMC data shows, the lowest annual tuition and fees for first-year veterinary students was $19,616 (North Carolina State University). The greatest was $72,292 (The Ohio State University).

Whatever numbers one opts to highlight, few in the veterinary community dispute that school debt is a big, unsolved problem for the profession.

'We are not living on an island'

Too big to expect one smallish profession to figure it out alone? Some say so.

"The one thing I always remind people is that we are not living on an island. We cannot pretend that we can fix this in [isolation]," said Dr. Caroline Cantner, a former assistant director for student initiatives at the AVMA, now serving as director for professional affairs at the AAVMC. (The two organizations, along with Michigan State, co-hosted Fix the Debt.) Cantner continued: "... the conversations are happening at a national level, a very high national level. It's within that context that we have to operate."

Educational debt relief has become a priority among progressive Democrats, and the Biden administration reportedly is reviewing the possibility of canceling a sum somewhere between $10,000 and $50,000 per borrower.

"The work that we do at AAVMC, and I know AVMA is doing as well, at the federal level is to make sure that our voice is heard and we are not an afterthought; that we're in this very large conversation that's happening," Cantner said.

Dr. Lisa Greenhill, senior director for institutional research and diversity at the AAVMC, notes that higher education tuition "is rapidly increasing across the board ... largely [as] the result of a public de-investment in education" that she said affects private and public institutions alike. Greenhill continued: "All medical education in general is particularly expensive .... MD programs are also rising at a rate of two times the Consumer Price Index, much like we see in DVM programs. ... [V]et med is not special when it comes to educational pricing, among other issues."

Dr. Tony Bartels, debt education director at the Veterinary Information Network, an online community for the profession and parent of the VIN News Service, sounded a similar theme. "The medical profession, the dental profession, they all want the same things, too, and they're a hell of a lot bigger than the veterinary profession," he said. "They can't get anything done. How are we going to get anything done?" Furthermore, the financial woes of people in relatively high-paying occupations aren't apt to elicit a lot of public sympathy, he said: "Nobody's playing the smallest little violin for health professionals."

Holland, the former SAVMA president, agrees that the veterinary community can't solve the debt problem by itself. Since graduating in 2017, he's spent some time in Washington D.C., working on Capitol Hill and at the U.S. Department of Agriculture. Today, he's a student advocate for VIN. Considering the summit in retrospect, Holland said, "I really wish policymakers had been involved, either from the local level or federal level."

Without support from policymakers, lawmakers and university decision-makers at the highest levels, he and Cantner said, veterinary schools' ability to reduce or temper the rise of tuition is limited.

"[I]n most cases, the deans do not even set their own tuition ..." Cantner said. "[L]et's say the schools go super lean and save a bunch of money, the president of the university may say, 'Great, thanks, I'll siphon the funding to the undergraduates.' ... [T]he mechanisms that determine funding are beyond the scope of the colleges of veterinary medicine themselves."

Some deans certainly try to contain costs. Dr. John Baker, who initiated Fix the Debt, is an example. Baker was dean of Michigan State from 2014 to 2018. During his tenure, he successfully advocated to his provost to minimize increases in tuition and even, to a degree, freeze it. Baker also found ways to pare program expenses — including his own reserved parking space — to free money for scholarships.

Now retired, Baker said he no longer is involved in the issue. "I hope some in the profession continue to address the student debt," he said.

Dr. Michael Chaddock, a former associate dean at Michigan State, was Baker's right-hand man in putting the summit together. Also retired, Chaddock is dismayed that the cost of schooling and the level of borrowing continue to rise. Then again, he noted, school leaders, as one of the working groups at the meeting, never committed to reducing expenses. Instead, they emphasized raising money for scholarships, a tactic he finds self-serving because the awards end up going to the schools.

"They have their hand out — to individuals, to alumni, to businesses, whoever," he said. "They say, 'Give us more money, and this is how we can help [students]. Give us more money, and then we, the college, can turn around and give more scholarships.' Which is a conflict of interest: 'Give us more money, and the students can pay us [with it].' It's a huge circle!"

Emphasizing that his opinions are his alone and do not represent any of the groups or institutions he's worked for, Chaddock also said the effort to fix the debt appears to have been watered down. Following the campaign's birth in Michigan, it was adopted by the AVMA, AAVMC and Veterinary Medical Association Executives and renamed the Veterinary Debt Initiative, or VDI.

"VDI — what does that say?" Chaddock asked in exasperation. "It doesn't say we want to fix it. It doesn't tell you any goals or anything. Maybe we don't want to call it Fix the Debt. Maybe we don't want to be accountable for anything."

Campaign shifts focus to the experience of debt

Cantner, AAVMC's debt-initiative point person, said the effort has shifted to the impact of debt on individuals' well-being and their perception of debt's effect on their lives.

She explained, "You could have two people with the same debt level, and one has a plan that they're comfortable with, that they're happy with, that they can meet their goals with, and they're fine. And the other one does not have [a] plan or is not happy with it." It's the "felt experience around the debt," she said, that is "really critical."

She elaborated: "We could get down to a certain number and still have people who feel they're in crisis. ... Our goal is to help with the experience of the debt." In short, she said, "My outcome is, how do you feel about your situation? And if you're cool, then that's great."

Cantner recognizes that those who want to see the debt-to-income ratio in better balance may be dissatisfied with that approach. "I know to the data folks, this feels like frou-frou, and 'you've gone off the rails,' " she acknowledged.

Turning to specific suggestions from the summit, she said that while all were well-intentioned, some would have minimal impact on the problem overall. Two examples:

- Scholarships. AAVMC data shows that 44% of veterinary students in 2020-21 received an average of $6,000 in scholarship funds. That is not a lot of money relative to the cost of schooling, and some awards are smaller, Cantner said. "If you spend three or four hours and you apply to 15 scholarships and you get one $500 award, do the math," she said. "Maybe you should have been doing something else — studying for anatomy or something."

- Shortening the period of schooling, and therefore the cost, by admitting students to veterinary school after one or two years of undergraduate work rather than the standard four. Cantner said most debt among new veterinarians is incurred in veterinary school, not during undergraduate studies. "So, how impactful is a strategy that potentially reduces undergraduate [costs]?" she asked.

Students learn financial savvy

Several recommendations from the summit involve sharpening students' awareness of money matters and business savvy. Some schools have taken the recommendations to heart. Michigan State, again, offers a case in point. In 2018, the school rolled into its core curriculum five semesters of professional skills, including career development, practice management and financial literacy, according to Dr. Donna Harris, who moderates the courses. Before, students were exposed to those topics in a single three-credit course their first year. Now they take five one-credit courses over 2½ years, receiving more information and time to absorb it.

"The first thing we talk about," Harris said, "is how to work with a budget or a spending plan as a student." Early on, some in class were unreceptive. On course feedback forms, they called it a waste of time, Harris recalled.

"I don't get any of those any more," she said. Apparently more aware of the price of entering their chosen profession, first-year students now arrive with greater financial savvy and are thankful to learn more, Harris said: "The assignment on developing a budget, they're so much better at it. They really think [it] through, and they are very grateful."

One key issue she raises with students is how to minimize their borrowing. First-year students especially are apt to take the maximum loan they can obtain through federal financial aid, having little sense of how much they'll truly need.

Harris explains that they have 120 days to return excess loan dollars without being charged interest. "I hear of students returning $5,000 and $10,000" for a single term, Harris said. "... I'm hoping that they gain some confidence after that first year and just don't take as much [from then on]."

Other topics covered in class include the expense of keeping pets — it would be best to hold off until they're out of school, Harris counsels — and how not to bust the bank on vacations. "Does it have to be a trip to the Caribbean, or can it be a hike in the woods? Or visiting friends?"

Some first-year students, upon realizing that they could be $250,000 in the hole by graduation, come to Harris in agony, asking whether they should drop out. If being a veterinarian is what they truly want, her answer is no. "I want the students to feel, OK, they can do this," she said.

She worries that the attention paid to the debt problem is, paradoxically, disempowering. "After we started raising the red flag about student debt, we had a significant number of people in the profession saying, 'Oh my gosh, we can't do this. Students can't do this.' When, in fact, they were doing this," she said. "Veterinarians are tremendously resilient, and they can do this. ... They are doing it. It doesn't mean it's OK, and it doesn't mean they should. But I don't want them to quit veterinary school."

Trying to 'tell a more complete story'

Bartels, the debt education director at VIN, spends his days guiding veterinary students and recent graduates through the thicket of managing student debt, providing one-on-one advice through VIN and VIN Foundation message boards, giving lectures to veterinary student and veterinarian audiences at schools and conferences around the country, and helping to build and maintain cost-of-education and debt-management tools available free through the VIN Foundation. Bartels comes by his expertise through personal experience: He and his wife, a veterinary internal medicine specialist, together owe $400,000-plus.

As someone coping with his own borrowing burden and who has counseled thousands of borrowers, Bartels is highly tuned to the nuances and complexity of debt. He dislikes the tendency of veterinary leaders and the media to simplify the numbers by using averages. When he does cite an average figure for debt, it's $204,675, which accounts for all educational debt of borrowers who graduated in 2020, not only the debt they incurred to pay for veterinary school.

"I use $204,675 a lot," Bartels said. "I use distributions a lot — debt by school, income by practice type, minimums and maximums, accounting for the things often unaccounted for in the discussion, like student loan interest, which can add more during veterinary school than some people borrowed for their entire undergraduate degree. Those figures tell a more complete story than a single average that lumps groups that shouldn't be lumped."

Understanding the nuances also can ease the added stress from owing more than the oft-quoted average, he said: "In my experience, it helps people to realize that they are not alone if they happen to have more debt than the average debt reported across all students, including zero-debtors."

Bartels also highlights the price differences among and within schools. In the nine years since he graduated from Colorado State University with dual DVM and MBA degrees, he's watched in dismay as veterinary education in the U.S. has skewed toward higher-priced seats.

The phenomenon is driven partly by the arrival of new private schools. In an AAVMC list of first-year tuition and fees charged by schools to residents of their states, from highest to lowest, three of the top six are among the newest programs in the country: Midwestern in Arizona (2014); Long Island University in New York (2020); and Lincoln Memorial University in Tennessee (2014). Like most private schools, they do not offer lower tuition for residents of their states.

Midwestern also stands out as having a high proportion of indebted graduates (99% in 2020) and the highest median debt among its borrowers ($347,415).

Solution of sorts or future fiasco?

In advising borrowers with heavy debt, Bartels recommends income-driven repayment, a lifeline offered by the government to federal student loan borrowers to keep their payments affordable. Participants pay no more than 15% of their discretionary income each month. The downside is that the payment may not fully cover the interest, let alone principal. If that happens, instead of shrinking, the balance grows.

After borrowers pay for 20 to 25 years, depending on their payment plan, the debt is discharged — the balance, forgiven. It is a happy ending with a hitch: Forgiven balances are considered by the government as income, subject to tax.

Bartels counsels borrowers how to choose the optimal loan repayment plan for their individual situation, how to save for the tax bill and how to prioritize other financial goals, like buying a house (he and his wife own two), buying a practice and preparing for retirement, all while managing student loans.

To the extent that students borrow more for education because government subsidizes education less, Bartels sees income-driven repayment as an after-the-fact public subsidy. In the absence of anything better, he considers it a solution to six-figure student debt because it lets borrowers avoid being crushed by the monthly payments. They just have to stomach watching the balance rise and assiduously plan for the tax.

Dicks, the former AVMA chief economist, is less upbeat about that strategy. "The shit hitting the fan has yet to happen," he predicted, meaning the tax. Now a consultant, Dicks doesn't believe borrowers, on the whole, will exercise the discipline required to save for decades and to resist the temptation to use the money for another purpose.

Whether that's true will not become clear for another 10-plus years. By Bartels' reckoning, the earliest an appreciable number of borrowers will reach forgiveness is 2032.

'Becoming a profession of privilege'

Dicks believes that the only true long-term solution is to revive a way of thinking about and funding education that worked well the past: "The way we laid it out in the Morrill Act of 1862 [which created the land-grant colleges] got it right," he said: "Ensure that citizens were educated in the areas needed by society ... to provide better solutions [for] society. America did that for more than 100 years, and the public benefits are seen everywhere.

"The recent change in philosophy to education being a means for higher income, and thus, those who ply that path should pay the costs, is having substantial and long-term deleterious social and personal impacts," Dicks said.

Absent such a shift in thinking, and absent an unforeseen slump in applicants to veterinary school, education costs and borrowing appear to be on a continued upward trajectory.

"It's really concerning," said Holland, the former SAVMA president, who graduated four years ago from the University of Illinois owing about $200,000.

Regarding his own debt, Holland is at peace. "I knew going in that this will follow me around awhile," he said. "If I owned a house, that would [also] be debt that hangs around for a while." And given the choice "between vet school and a house, I would rather have the degree," he said.

What concerns him more are debt's effects on the profession. Veterinary school "is exorbitantly expensive, and it's becoming a profession of privilege, which is not what I think anybody wants," Holland said.

Although the goal of Fix the Debt is far from achieved, he doesn't fault the quality of the effort. "If it were really that easy to fix," Holland mused, "it would be fixed by now."

Jennifer Fiala contributed to this report.

Part 2: Purdue shows freezing price of veterinary school is possible

Part 3: Three 'zero debtors' in veterinary school speak